Public Charities vs. Private Foundations: Understanding the Key Differences

Public Charities vs. Private Foundations: Understanding the Key Differences

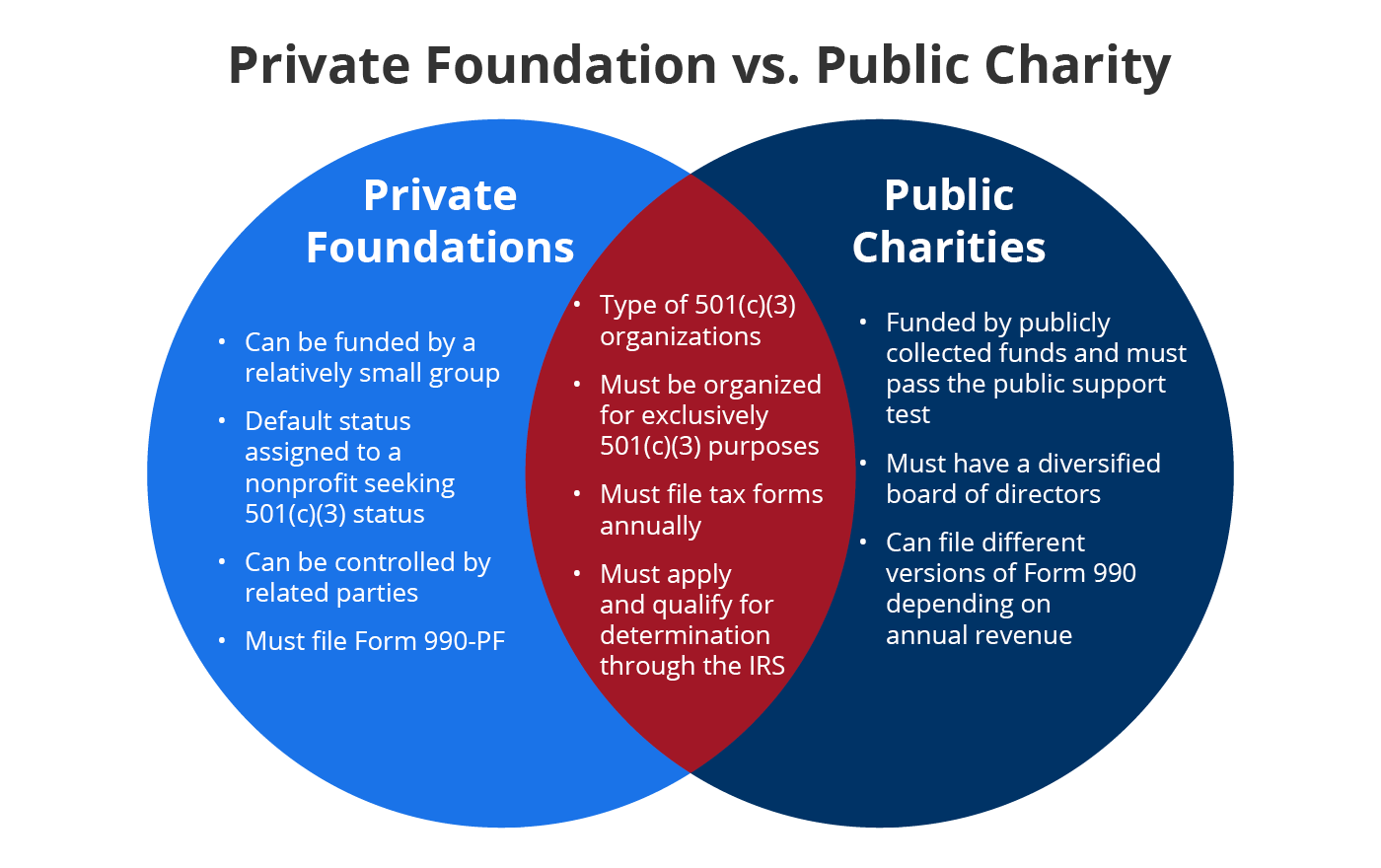

When it comes to nonprofit organizations, two primary categories exist: public charities and private foundations. While both operate under the 501(c)(3) tax-exempt status, they have significant differences in terms of funding, governance, and operations. Understanding these distinctions is crucial for donors, founders, and nonprofit professionals who want to make informed decisions about charitable giving and organizational structure.

Definition & Purpose

Public Charities

A public charity is an organization that receives the majority of its funding from the general public, government grants, or a broad base of donors. These nonprofits often focus on direct services, advocacy, education, and religious activities. Examples include food banks, museums, universities, and places of worship. Public charities typically engage in community-oriented initiatives and rely on widespread support to sustain their programs.

Private Foundations

A private foundation, on the other hand, is typically funded by an individual, a family, or a corporation. Instead of directly providing services, foundations primarily make grants to support other charitable organizations. Private foundations often have a long-term vision, focusing on philanthropy and sustainable funding for various causes. Examples include the Bill & Melinda Gates Foundation and the Ford Foundation. These organizations use their endowments to fund initiatives that align with their mission.

Funding Sources

Public Charities:

- Depend on donations from individuals, businesses, and government sources.

- Must meet the IRS public support test, ensuring that at least one-third of their revenue comes from diverse public contributions.

- Often conduct fundraising events and campaigns to sustain their operations.

- Can apply for federal and state grants to support their projects.

- May receive corporate sponsorships and foundation grants to expand their reach.

Private Foundations:

- Funded primarily by an individual, family, or corporation.

- Generate revenue through investments and endowments rather than ongoing public fundraising.

- Required by the IRS to distribute at least 5% of their assets annually to charitable causes.

- Often establish donor-advised funds to facilitate charitable giving over time.

- Have the flexibility to fund niche causes or long-term initiatives that may not fit within traditional public charity models.

Tax Treatment & Deductibility

Public Charities:

- Donations to public charities are tax-deductible up to 60% of an individual’s adjusted gross income (AGI).

- Less stringent excise tax regulations compared to private foundations.

- Eligible for sales tax exemptions in many states, reducing operational costs.

- Do not pay federal income taxes but must comply with annual reporting requirements.

- Encouraged to reinvest a significant portion of their funds back into their programs and services.

Private Foundations:

- Donations are tax-deductible up to 30% of an individual’s AGI.

- Subject to an excise tax (1-2%) on investment income.

- Must adhere to strict IRS guidelines to avoid conflicts of interest.

- Limited in their ability to conduct direct charitable activities, focusing instead on funding other organizations.

- Can establish long-term investment strategies to ensure financial sustainability and growth.

Governance & Compliance

Public Charities:

- Governed by a diverse board of directors that is independent from the organization’s founders.

- Must regularly file IRS Form 990 to report financial and operational details.

- Subject to more public scrutiny due to their reliance on donations.

- Required to follow specific governance policies, including conflict-of-interest policies and financial transparency regulations.

- Encouraged to conduct annual audits to maintain donor confidence and regulatory compliance.

Private Foundations:

- Often governed by a small board, typically including family members or close associates.

- Must file Form 990-PF, which provides more transparency regarding grants and expenses.

- Restricted from excessive insider transactions to prevent conflicts of interest.

- Can create multi-generational leadership structures, allowing families to manage charitable giving over several decades.

- Must ensure all grant distributions align with their tax-exempt purpose to avoid penalties.

Grantmaking vs. Direct Services

Public Charities:

- Provide direct services to individuals and communities.

- May operate hospitals, schools, shelters, and other service-based programs.

- Can engage in limited lobbying but must be cautious about political activities.

- Often host community outreach programs, disaster relief efforts, and health initiatives.

- Rely on volunteers and grassroots support to drive their impact.

Private Foundations:

Primarily focus on grantmaking to support other nonprofits.

Cannot engage in lobbying or political campaigning.

Have greater flexibility in funding specific initiatives, scholarships, and research programs.

May establish long-term partnerships with universities, research institutions, and global aid organizations.

Can fund innovation and experimental projects that may not receive traditional public charity support.

Which One Is Right for You?

If you’re considering starting a nonprofit or donating to one, choosing between a public charity and a private foundation depends on your goals:

If you want to actively raise funds and provide direct community services, a public charity may be the best fit.

If you or your family want to donate a large sum and oversee grant distribution to various causes, a private foundation might be more suitable.

Those interested in hands-on involvement with beneficiaries may find public charities more fulfilling.

Individuals or corporations looking to create a long-term philanthropic legacy may prefer the structure of a private foundation.

Donors should also consider the tax implications and governance responsibilities associated with each type of nonprofit.

Conclusion

Both public charities and private foundations play critical roles in philanthropy, but they operate under different rules and structures. Public charities focus on fundraising and service delivery, while private foundations concentrate on grantmaking and long-term funding strategies. Understanding these distinctions ensures better decision-making for donors, nonprofit leaders, and anyone interested in charitable giving.

If you’re considering forming a nonprofit or foundation, consulting with a legal or financial expert can help ensure compliance with IRS regulations and effective organizational management. Taking the time to understand these differences can lead to more impactful charitable work and greater benefits for the communities these organizations serve.